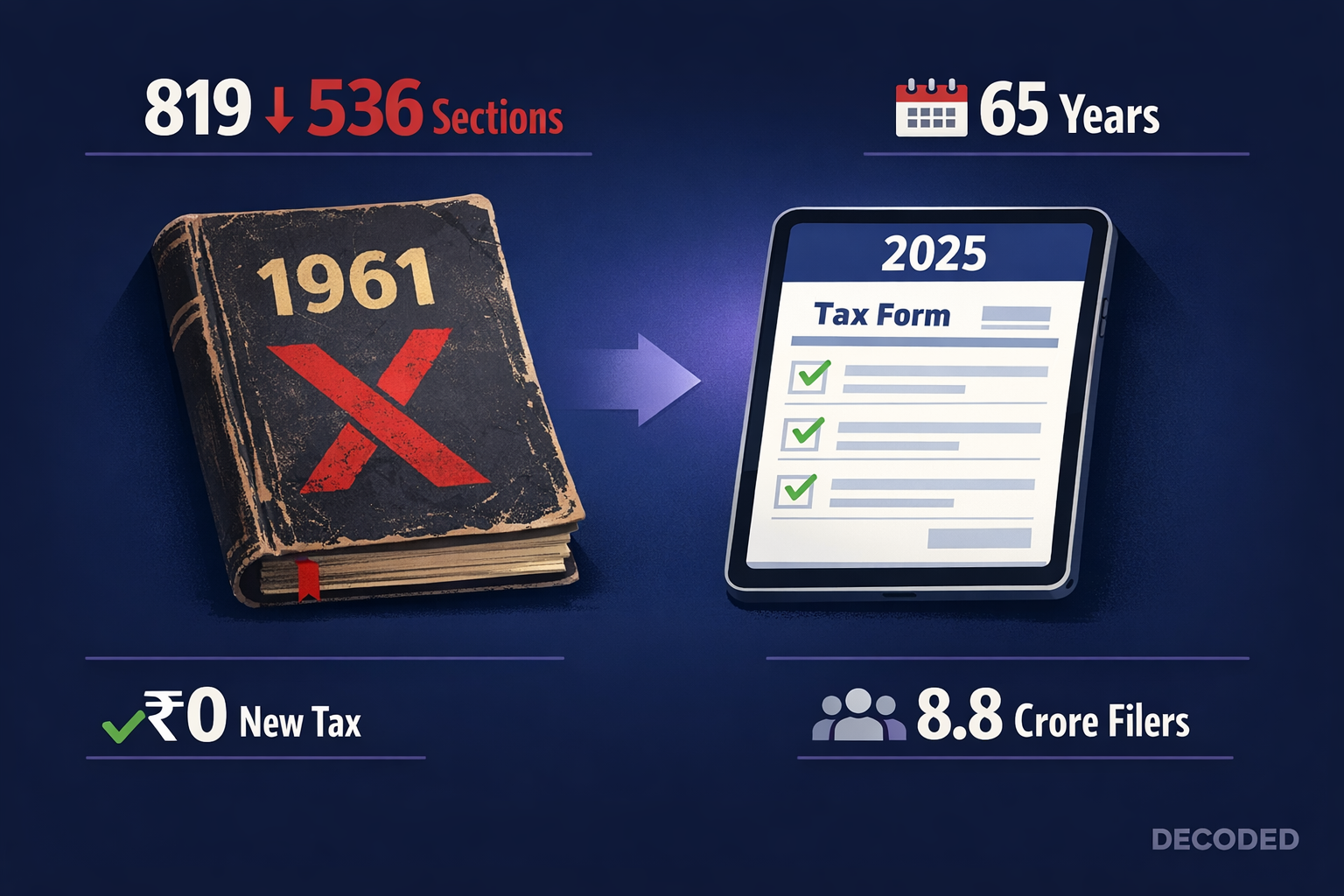

At midnight on April 1, 2026, India did something it has never done before: it retired an entire piece of tax legislation and replaced it with a new one.

The Income Tax Act, 1961 — the law under which every Indian has filed taxes for six decades — is officially dead. In its place: the Income Tax Act, 2025. 536 sections. 23 chapters. Same tax rates.

Wait, same tax rates? Yes. Not one rupee more. Not one rupee less. So what exactly changed?

The Income Tax Act 2025 is explicitly revenue-neutral. The government was clear about this from the start: this is not a tax increase, a tax cut, or a policy shift. It is a structural rewrite of a law that had become unreadable.

Think of it this way: imagine your apartment has the same plumbing from 1961. The water still flows, but every repair over 65 years added new pipes, connectors, and bypasses. The new Act isn't changing your water supply — it's replacing the pipes with modern plumbing. Same water. Cleaner system.

Here's what the rewrite looks like by the numbers:

| Metric | Old Act (1961) | New Act (2025) | Change |

|---|---|---|---|

| Total sections | 819+ | 536 | -35% |

| Chapters | 47 | 23 | -51% |

| Provisos | ~1,200 | Removed (absorbed into plain language) | -100% |

| Explanations | ~900 | Removed | -100% |

| TDS sections | 60+ (Sec 192–194T) | 3 sections | -95% |

| Legislative volume | Baseline | ~40% smaller | -40% |

| Tax slabs & rates | Unchanged | Unchanged | 0% |

The most common criticism of the new Act is also its most honest description: it's the same law in a new suit. Tax rates haven't changed. Deductions haven't changed. The old tax regime and new tax regime both continue to exist side by side.

But here's what did change — and some of these changes are significant, even if they don't show up on your tax calculation:

The "Tax Year" SwitchFor 65 years, Indians have dealt with two confusing terms: Previous Year (the year you earn income) and Assessment Year (the year you file the return). Income earned in "FY 2025-26" was assessed in "AY 2026-27." Two different names for what is functionally the same 12-month period.

The new Act replaces both with a single concept: Tax Year. It's the April-to-March period in which you earn income — and the year under which you file your return. One label. One period. Done.

This may sound cosmetic. It isn't. Every government form, software, employer payslip, bank TDS certificate, and mutual fund statement referred to "FY" or "AY." That terminology is now obsolete. Your Form 16 is now Form 130. Your Form 26AS (the annual tax statement) is now Form 168. Your Form 12BB (investment declaration to employer) is now Form 124.

15 Rules That Changed at Midnight. Before vs After.Here's every major change, in one table. Bookmark this.

| What Changed | Before (Act 1961) | After (Act 2025) | Who's Affected |

|---|---|---|---|

| Tax Year terminology | Previous Year + Assessment Year | Single "Tax Year" | Everyone |

| Children education allowance | ₹100/month per child | ₹3,000/month per child | Salaried parents |

| Hostel allowance | ₹300/month per child | ₹9,000/month per child | Salaried parents |

| Meal exemption | ₹50 per meal | ₹200 per meal | Salaried employees |

| Non-cash gifts | ₹5,000/year exempt | ₹15,000/year exempt | All employees |

| HRA 50% exemption cities | Delhi, Mumbai, Kolkata, Chennai only | + Bengaluru, Pune, Hyderabad, Ahmedabad | Salaried (old regime) |

| HRA landlord PAN | Required above ₹1L/year | Mandatory with detailed disclosure | HRA claimants |

| STT on futures | 0.02% | 0.05% (2.5x increase) | F&O traders |

| STT on options | 0.1% | 0.15% (1.5x increase) | F&O traders |

| TCS on overseas tours | 5% (up to ₹10L), 20% (above) | Flat 2% | Travelers abroad |

| TCS on education remittance | 5% | 2% | Students abroad |

| Buyback tax | Taxed as deemed dividend (company pays) | Taxed as capital gains (shareholder pays) | Investors |

| SGB redemption | Tax-free for all holders | Tax-free only for original subscribers | SGB secondary buyers |

| MAT rate | 15% | 14% (made final tax) | Companies |

| ITR-3/4 deadline | July 31 | August 31 | Business owners, freelancers |

| Overseas medical treatment | Tax-free if income < ₹2L | Tax-free if income < ₹8L | Employees seeking treatment abroad |

If you're a salaried employee, most of the changes work in your favor. The education allowance jump from ₹100 to ₹3,000 per month is meaningful for parents — that's ₹36,000 per year per child that's now tax-exempt, up from ₹1,200. Hostel allowance went from ₹300 to ₹9,000 per month — a 30x increase. Meal exemptions quadrupled from ₹50 to ₹200 per meal.

If you live in Bengaluru, Pune, Hyderabad, or Ahmedabad and claim HRA under the old tax regime, you now qualify for the 50% exemption that was previously reserved for Delhi, Mumbai, Chennai, and Kolkata. This could save you ₹20,000-50,000 per year depending on your rent.

The mandatory landlord PAN requirement for HRA claims above ₹1 lakh per year is not a new burden — it's closing a long-standing loophole. With PAN linked to Aadhaar and nearly universal among adults with bank accounts, providing your landlord's PAN is a basic compliance step. If you were claiming HRA without a verifiable landlord, this change asks you to do what you should have been doing all along.

Business Owners & Freelancers: MixedThe extension of the ITR-3 and ITR-4 filing deadline from July 31 to August 31 is a genuine quality-of-life improvement. An extra month to finalize books of accounts before filing makes a real difference for small business owners who often scramble in July.

The MAT rate reduction from 15% to 14%, with MAT becoming a final tax (no more credit carryforward), simplifies things for companies but removes a future benefit. For MSMEs, the compliance architecture hasn't fundamentally changed — you still need a CA for tax audits above the threshold.

F&O Traders: Clear LoserThe STT hike on futures (0.02% to 0.05%, a 2.5x increase) and options (0.1% to 0.15%) directly increases the cost of speculative trading. This is intentional — the government wants to discourage retail investors from heavy F&O speculation where 9 out of 10 individual traders lose money. Whether you see this as protection or punishment depends on which side of the P&L you sit.

Students & Travelers Abroad: Clear WinnerTCS on overseas tour packages crashed from a complex 5%-20% slab to a flat 2%. For education remittances, TCS dropped from 5% to 2% with no threshold limit. If you're sending ₹20 lakh for a child's education abroad, your upfront TCS dropped from ₹1,00,000 to ₹40,000 — a ₹60,000 improvement in immediate cash flow. (The TCS is adjustable against your final tax, but the upfront burden matters.)

Farmers: No ChangeAgricultural income remains fully exempt from income tax under both the old and new Acts. This is constitutionally protected and wasn't touched by the rewrite. Farmers who also have non-agricultural income (salary, business) will notice the form-number changes, but their agricultural exemption is intact.

Can You File Your Own Taxes Now? The Self-Filing Reality Check.This is the question everyone asks but few sources answer honestly. Here's the reality, by category:

| Taxpayer Type | Self-Filing Possible? | What's Changed |

|---|---|---|

| Salaried (simple) | Yes — easier now | Form 168 (new AIS) auto-populates income, TDS, investments from PAN. Nearly pre-filled. |

| Salaried (HRA, multiple incomes) | Yes, but needs care | HRA requires landlord PAN documentation. AIS cross-checks — mismatches trigger NUDGE notices. |

| Freelancer (under audit threshold) | Possible, not recommended | Filing deadline extended to August 31. Still complex for multiple income streams. |

| Business owner (audit required) | No — CA mandatory | Tax audit restricted exclusively to CAs. CMAs and CS excluded under new Act. |

| Investor (stocks, MF, SGB) | Possible with tools | Buyback and SGB rules changed. Capital gains reporting auto-populated from broker data. |

The new Form 168 (replacing Form 26AS) is the game-changer for self-filing. It's India's version of what Australia's ATO has done for years: auto-populate your return with data the government already has from employers (via TDS), banks (via interest reporting), brokers (via STT), and mutual funds. If the pre-filled data is accurate, filing becomes a review-and-submit process rather than a build-from-scratch exercise.

The new Act isn't all plumbing upgrades. There are three areas where experts have raised legitimate concerns:

1. Re-Litigation RiskThe old Act has been interpreted by courts for 65 years. Thousands of rulings have settled ambiguities in the law. The new Act rewrites provisions in new language and assigns new section numbers — meaning old precedents may not directly apply. As PRS India noted, "redrafting certain provisions may lead to re-litigation of settled issues." Tax professionals will spend years mapping old rulings to new sections.

2. Search & Seizure PowersThe new Act retains and extends search-and-seizure powers to include "electronic media or computer systems" — covering emails, social media accounts, and cloud storage. This power existed informally, but the new Act codifies it explicitly. Critics note there is no additional judicial oversight requirement for accessing digital data, raising privacy concerns.

3. The NUDGE Problem (Teething, Not Terminal)The CBDT's NUDGE campaign, launched in December 2025, uses automated AI-driven analysis to flag potential under-reporting. It has already caused significant delays: as of February 2026, 63 lakh returns remain pending processing, with 24.64 lakh delayed beyond 90 days.

But context matters. Every country that modernized its tax system went through this.

| Country | Tax Modernization | Teething Period | Outcome |

|---|---|---|---|

| UK (HMRC) | Making Tax Digital | 8 years of delays (2018 target, launching April 2026). 94% of businesses still unprepared. | Still in progress. HMRC admitted it "underestimated the complexity." |

| Australia (ATO) | Pre-filled returns + Single Touch Payroll | 2-3 years to mature data accuracy | Success — most Australians get pre-filled returns by July. Widely adopted. |

| India | AIS + Form 168 + NUDGE | Year 1. 63L returns pending. | In progress — same trajectory as Australia. |

India's AIS auto-population system follows Australia's proven model. The NUDGE delays are growing pains of a system learning to cross-check data at scale — not evidence of a broken system. The UK took eight years and still isn't fully live. India launched an entirely new Act and digital infrastructure simultaneously. Some turbulence is expected.

What Supporters Say

- 40% reduction in legislative volume makes the law more accessible to non-lawyers

- Auto-populated returns (Form 168) reduce errors and CA dependency for simple returns

- TCS cuts on education and travel directly benefit middle-class families

- Extended filing deadlines give business owners breathing room

- Mandatory landlord PAN closes a genuine evasion loophole

What Critics Argue

- Language "simplification" is cosmetic — "irrespective of" isn't simpler than "notwithstanding"

- 65 years of settled case law may need re-litigation under new section numbers

- Search powers expanded to digital data without judicial oversight

- Every CA, software, and form reference needs updating — massive transition cost

- NUDGE campaign already causing refund delays for honest filers

The government has not explicitly promised faster refunds under the new Act. But the infrastructure should logically lead there: better data matching (AIS) means fewer manual reviews, which should mean faster processing.

The current reality, however, is moving in the opposite direction — temporarily. The NUDGE campaign has created a bottleneck where automated scrutiny catches more cases, but processing capacity hasn't scaled proportionally.

| Refund Metric | Target | Current Reality (Feb 2026) |

|---|---|---|

| Processing time after e-verification | 16-18 days | 4-8 weeks (many cases) |

| Pending returns | — | 63 lakh still processing |

| Returns delayed beyond 90 days | 0 | 24.64 lakh |

| Legal deadline to process | — | December 2026 (9 months from year-end) |

The expectation is that by the second or third filing cycle under the new Act (2027-28), the system will stabilize. Australia's ATO went through the same curve — early years of pre-filling had data accuracy issues, but within 2-3 cycles, the system became reliable enough that most taxpayers could file in under 30 minutes.

What You Need to Do. Right Now.- Your employer will issue Form 130 (not Form 16) for Tax Year 2026-27

- If claiming HRA, keep your landlord's PAN ready (mandatory if rent exceeds ₹1L/year)

- Check your Form 168 (new AIS) on the income tax portal after June — verify all data is accurate before filing

- Filing deadline remains July 31, 2027 for salaried individuals

- Your ITR-3/ITR-4 deadline is now August 31 — one extra month

- TDS deductions from April 1 follow Section 392(1) of the new Act (not old Section 192)

- Ask your CA for the section mapping guide (ICAI has published old-to-new section comparisons)

- All references in contracts, invoices, and compliance docs citing old section numbers need updating

- F&O trading cost increased: STT on futures 0.02% → 0.05%, options 0.1% → 0.15%

- Share buybacks now taxed as capital gains in your hands — not at the company level

- If you hold SGBs bought from the secondary market, redemption is no longer tax-free

- Capital gains auto-populated from broker data via AIS — verify before filing

- TCS on overseas tour packages dropped from 5-20% to flat 2%

- TCS on education remittances dropped from 5% to 2% with no threshold

- TCS is adjustable against your final tax liability — claim it when you file

The Bottom Line

The Income Tax Act 2025 is not a revolution — it's a renovation. Same tax rates, same deductions, same regimes. But the plumbing is genuinely better: 40% less legislative volume, auto-populated returns, and a single "Tax Year" concept that eliminates decades of confusion. The real test isn't whether the law looks simpler on paper — it's whether a salaried employee in Bengaluru can file an accurate return in 30 minutes without paying a CA. If Australia's experience is any guide, India is about 2-3 filing cycles away from that reality. The teething problems — NUDGE delays, form-number chaos, re-litigation risk — are real but temporary. Every country that modernized went through this. The important thing is that India started.