March 7, 2026: Domestic LPG hiked ₹60. First increase in 11 months. Delhi: ₹913. Commercial cylinders: up ₹115.

March 11, 2026: Day 11 of the Iran war. The US declares its "most intense day of strikes." 10,000 civilian sites bombed. Hormuz still closed. 200+ ships stranded. India has ~10 days of LPG left. And the government says everything is "comfortable."

If you cook with gas — and 31 crore Indian families do — this story is about you. The ₹60 hike on March 7 was the first domestic increase in 11 months, and analysts warn it may not be the last. If Brent crude stays above $87 and the Hormuz blockade continues, cylinders could cross ₹1,000 before the financial year ends.

But LPG is only the beginning. Every $10 per barrel rise in crude oil adds 20-30 basis points to India's inflation and widens the import bill by $12-15 billion annually. Brent has already risen 37% in 2026. On March 2, the Sensex crashed 2,743 points intraday, wiping out ₹6.8-8 lakh crore. Container shipping costs have doubled from $1,800 to $3,800, and 400,000 tonnes of basmati rice are stuck at ports.

This isn't just energy. It's food, transport, manufacturing, and livelihoods. The Middle East accounts for 17% of India's exports, 55% of its crude, and 38% of its remittance inflows — $51.4 billion from the Gulf diaspora. All of it is now at risk.

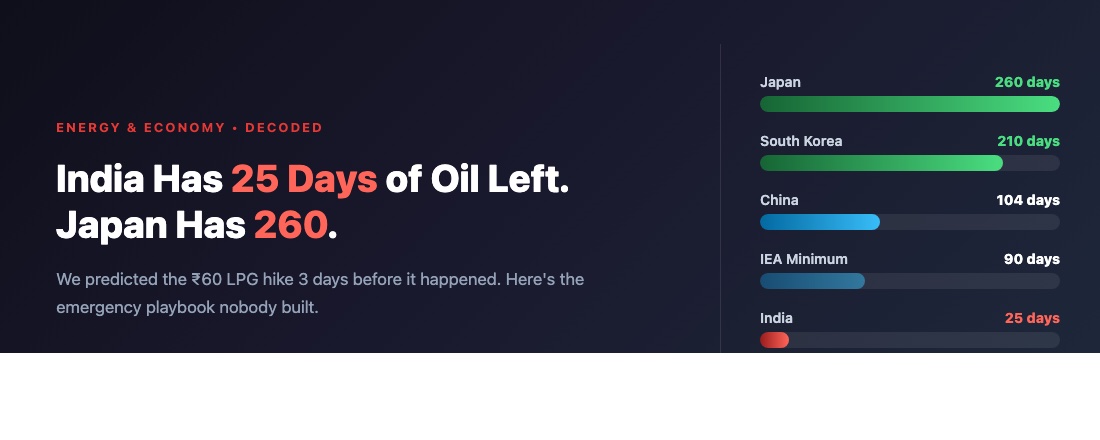

10 Days of LPG. 9.5 Days of Reserves. "Comfortable."Petroleum Minister Hardeep Singh Puri says India is in a "very comfortable position" with "no cause for worry." Here's what "comfortable" actually looks like, compared to countries that actually prepared:

| Country | Reserve Days | How They Built It |

|---|---|---|

| Japan | 260 days | Govt + industry + joint storage with Saudi, UAE, Kuwait |

| South Korea | 210 days | Govt 76M barrels + private 74M barrels + 52 days LNG |

| United States | 200 days | Strategic Petroleum Reserve + shale production surge |

| China | 104 days | Massive state reserves + EV transition reducing demand |

| Germany | 90 days | IEA-mandated minimum + EU solidarity mechanisms |

| India | 25 days | SPR 9.5 days + commercial stocks. No industry mandate. |

The IEA requires member states to maintain 90 days minimum. India isn't even at 30. Japan didn't build 260 days overnight — it took decades of deliberate policy: government stocks managed by JOGMEC, compulsory industry stockholding, and a brilliant innovation — joint oil storage agreements with Saudi Aramco, ADNOC (UAE), and Kuwait. Gulf producers keep oil physically stored in Japan. In return, they get strategic Asian market access. Japan gets reserves. India has zero such agreements.

Here's the number that explains everything: oil transiting Hormuz represents just 6.6% of China's total energy consumption. For India, the Middle East supplies 55% of crude imports. This isn't just about reserves — it's about structural dependency.

| Indicator | India | China | Japan |

|---|---|---|---|

| Oil import dependence | 88.6% | ~72% | ~90% |

| Oil demand trend | Rising fastest globally | Declined in 2024 | Declining |

| EV share of new car sales | 10% | 50% | ~25% |

| Nuclear share of electricity | 3% | 5% | 8% |

| Reserve days | 25 days | 104 days | 260 days |

| Hormuz dependency | 55% of crude | 6.6% of energy | ~80% of crude |

China's oil demand declined for the first time in 20 years in 2024 — driven by EVs. Half of all cars sold in China are electric, displacing 0.43 million barrels per day of gasoline. By 2030, China will account for 57% of global EVs. Its dependency on oil is structurally shrinking.

India went the other direction. Oil import dependence climbed to 88.6% in FY26 — the highest ever. Domestic production is lagging. India is now the world's top incremental oil demand driver, surpassing China. Japan has even higher import dependence (90%) but compensated with 260 days of reserves. India has neither declining demand nor adequate reserves.

3 Decades. 3% Nuclear. Zero Thorium Reactors.India sits on the world's largest thorium reserves. The three-stage nuclear program was envisioned in the 1950s by Homi Bhabha as India's path to energy independence. Seven decades later: nuclear provides 3% of electricity from 8,880 MW of capacity. The Prototype Fast Breeder Reactor (PFBR) — the bridge to thorium — is still being commissioned after decades of delays. Full thorium exploitation won't happen before 2050.

Meanwhile, the solar story is brighter: 180 GW installed, 9% of electricity. But solar and wind are intermittent — coal still provides 70% of power generation. And renewables don't solve the oil problem. Transport, cooking gas, petrochemicals — these run on hydrocarbons. You can't charge an LPG cylinder with a solar panel.

The EV gap is where it hurts most. India is at 10% EV penetration. China is at 50%. Every electric car sold in China is one less barrel of oil imported. India's 2030 target is 30% EV sales — ambitious, but it was supposed to be the 2025 target before being pushed back. The structural oil demand reduction that China achieved through aggressive EV policy is something India hasn't even started meaningfully.

$370 Million in Iran. $1.18 Billion in Israel. Both Burning.India has major strategic infrastructure in both warring nations — a position no other country of India's scale occupies:

| Asset | Investment | Strategic Purpose | Status Now |

|---|---|---|---|

| Chabahar Port (Iran) | $370M (10-yr deal) | Bypass Pakistan, connect Central Asia via INSTC | Funding frozen in 2026 budget |

| Haifa Port (Israel) | $1.18B (Adani) | IMEC corridor gateway to Europe | War zone, physical security at risk |

India built two trade corridors through the Middle East: the INSTC (via Iran and Russia) and IMEC (via Israel, UAE, Saudi Arabia to Europe). Both are now compromised by the same conflict. The INSTC depends on Iran's stability. IMEC depends on Israel's security. When both sides are at war, both roads catch fire simultaneously.

Modi's diplomacy has kept Chabahar operational through the conflict — a genuine achievement. But the structural vulnerability remains. Only China plays a similar "both sides" game with Iran ($400B deal under discussion) and Israel (tech investment hub). The difference? China does it with 104 days of reserves and declining oil dependence. India does it with 25 days and rising dependency.

Government Position

- "No shortage of energy. No cause for worry." — Minister Puri

- 100M barrels across SPR + commercial + tankers = 40-45 days cover

- Diversified to 40+ crude suppliers (from 27 a decade ago)

- Russian crude pivot post-2022 was brilliant and worked

- US waiver for Russian oil shows diplomatic leverage

What Analysts Say

- 10 days of LPG stocks is not "comfortable" for 31 crore families

- 40-45 days total includes oil already on tankers — not all accessible

- SPR alone is 9.5 days. Japan's SPR alone is 146 days.

- OMCs absorbing losses — unsustainable above $90 Brent

- 88.6% import dependency is rising, not falling

The 30-day Russian oil waiver expires on April 4. It only covers oil that was already loaded before March 5. This is not a policy shift — it's a one-time emergency patch. If the war continues:

| Scenario | Brent Oil | Impact on India |

|---|---|---|

| War ends in 2-4 weeks | $75-80 | LPG stabilizes at ₹913. Limited further damage. |

| War continues, Hormuz partially reopens | $85-95 | Petrol/diesel hike likely. LPG could hit ₹950-1,000. OMCs bleed. |

| Prolonged conflict, Hormuz stays closed | $100+ | LPG crosses ₹1,000. Petrol crosses ₹120. Inflation spirals. Current account deficit widens sharply. |

| Conflict extends 6+ months | $100-120 | $51.4B Gulf remittances at risk. GDP growth hit by 0.5-1%. Possible rationing. |

India has already invoked emergency powers to prioritize 4 key sectors for remaining natural gas. The government ordered refiners to divert propane and butane from petrochemicals to LPG production. These are crisis measures, not policy — they buy weeks, not months.

Plot Twist: The 5-Year Fix Japan Proved WorksIndia's energy crisis isn't unsolvable. It's just unsolved. Every tool exists. Other countries used them. Here's the practical roadmap, organized by what can be done now versus what should have started a decade ago:

Immediate: 0-6 Months1. Copy Japan's joint storage model. Saudi Aramco, ADNOC, and Kuwait already store oil in Japan under bilateral agreements — Japan covers rent, Gulf producers get Asian market access, and Japan gets priority supply during crises. ADNOC already leases space in India's existing SPR. Expand this to Saudi and Kuwait immediately. Each deal adds 5-7 days of cover at minimal cost.

2. Fast-track LPG contracts outside the Gulf. India signed a 2.2 million tonne/year LPG contract with US Gulf Coast suppliers in November 2025 — a smart move. Replicate with Australia, Algeria, and Nigeria. Target: reduce Hormuz LPG dependence from 85% to 60% within 18 months.

3. Complete SPR Phase 2. The Chandikhol (Odisha) and Padur expansion will add 6.5 million metric tonnes. Push completion from "planned" to "under construction" status. Every month of delay is a month of vulnerability.

Medium-term: 1-3 Years4. EV moonshot. China hit 50% EV sales through aggressive policy — subsidies, charging infrastructure, manufacturing incentives. India is at 10%. The FAME III scheme needs to be 3x the scale of FAME II. Every EV sold is one less barrel imported. Target: 30% by 2030 — and mean it this time.

5. Mission Samudra Manthan. India currently drills about 30 deepwater exploration wells per year. The plan is to scale to 100 wells per year. This is the single biggest lever for reducing import dependence long-term. It needs funding, regulatory clearance, and political will — all three simultaneously.

6. Nuclear fast-track. Stop waiting for thorium (2050+). Deploy proven reactor designs now. Small Modular Reactors (SMRs) can add distributed nuclear capacity faster and cheaper than traditional plants. Target: from 8.8 GW to 22.5 GW by 2031 — the government's own stated goal, currently far behind schedule.

Long-term: 3-10 Years7. Build a third trade corridor. Both IMEC (via Israel) and INSTC (via Iran) are compromised by the same conflict. India needs a corridor that doesn't go through the Middle East at all — an Africa corridor or Central Asian overland route. Diversification of routes, not just sources.

8. 500 GW non-fossil by 2030. India's own target. Solar + wind + nuclear + hydro. An 80% clean grid by 2040. Every megawatt of clean electricity reduces the burden on imported fossil fuels. The estimated investment needed: $1.5 trillion between 2026-2035 (Wood Mackenzie).

The ₹1.5 Trillion Question

The cost of building energy security is $1.5 trillion over a decade. The cost of not building it? We're watching it right now — ₹60 per cylinder hikes, ₹6.8 lakh crore stock market crashes, 400,000 tonnes of rice rotting at ports, and a government ordering emergency LPG rationing. Every major Middle East conflict will hit India's kitchen first. The question isn't whether India can afford to build resilience. It's whether it can afford not to.

The Strait of Hormuz is one of five maritime chokepoints through which 70% of global oil demand passes:

| Chokepoint | Oil Flow | India Exposure | Conflict Risk |

|---|---|---|---|

| Strait of Malacca | 24M bpd | High — SE Asian crude | China-Taiwan, piracy (up 280% in 2025) |

| Strait of Hormuz | 20M bpd | Critical — 55% of crude | Active war (now) |

| Suez Canal | 9M bpd | Medium — Europe route | Houthi attacks (2024-25) |

| Bab el-Mandeb | 8M bpd | Medium — Red Sea | Yemen conflict, piracy |

| Turkish Straits | 3.5M bpd | Low | Russia-NATO tensions |

India is exposed to the top two simultaneously. If the Strait of Malacca were disrupted — by a China-Taiwan conflict, or the piracy surge that saw incidents rise 280% in 2025 — India would lose another supply line. Two chokepoint disruptions at once, with 25 days of reserves? That's not a scenario anyone has planned for.

The pattern is clear. Red Sea disruptions in 2024. Hormuz in 2026. The question is never if the next chokepoint closes, but when. And with every disruption, countries with reserves and diversified energy ride it out — while India scrambles.

The Bottom Line

The Iran war is 7,000 km from India. Your kitchen is 0 km. India imports 88.6% of its oil, depends on one strait for 80-85% of its LPG, and has 25 days of reserves in a world where Japan has 260. The Russian oil pivot of 2022 was brilliant — for crude. But it left LPG, LNG, and long-term structural dependency untouched. China is reducing its oil addiction through EVs. Japan stockpiled a year's worth of buffer. India did neither. The ₹60 hike isn't the crisis. It's the symptom. The crisis is that after seven decades of oil dependence, India still doesn't have a Plan B for 31 crore kitchens. Building one will cost $1.5 trillion over a decade. Not building one will cost more — every single time a strait closes, an oil price spikes, or a war breaks out 7,000 km away and arrives at your stove the same week.